How Washington Is Compressing China’s Strategic Headroom

A co-ordinated squeeze on energy supply, maritime access, critical minerals, proxy defence credibility, and allied cohesion — and the investment implications.

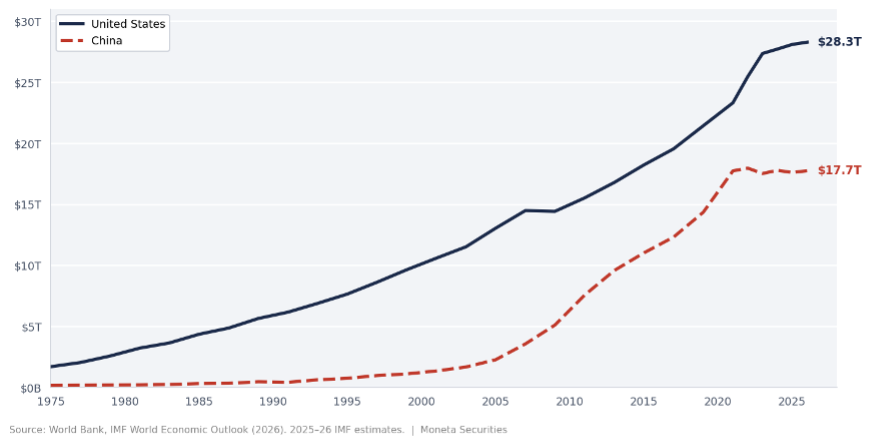

China’s nominal GDP trajectory broke in 2021 and has not recovered. At $17.7 trillion, it sits 60% below US nominal output and the gap is widening. The standard explanation; a property sector in multi-year contraction, deflationary pressure, an export-dependent economy facing tariff headwinds, is accurate. It is also incomplete.

What the domestic narrative omits is the degree to which China’s external constraints have been systematically tightened across the same period. The three sources of sanctioned crude that powered its independent refinery sector have been disrupted within eighteen months. Its seaborne energy runs through maritime chokepoints under US and allied naval dominance; a structural vulnerability that was live-tested in early 2026 for the first time. A US-led mineral diplomacy campaign is contesting not just China’s primary supply positions but the circumvention architecture China built to work around them. NATO’s burden-sharing commitments have reached their highest level in the alliance’s history. And Canada, the largest US trading partner, arrived at CUSMA renegotiation having publicly broken from Western EV tariff alignment to secure an agricultural concession from Beijing, handing Washington a negotiating lever it will use.

These pressures compound China’s domestic structural weaknesses rather than operating independently of them. This report examines each vector, their interaction, and the investment implications.

Figure 1: US vs. China Nominal GDP (USD billions), 1975–2026E. Source: World Bank; IMF World Economic Outlook 2026.

| Vector | Mechanism | China Impact | Status |

| Venezuela | 25% tariff on buyers; Maduro removal | ~600 kbpd disrupted; teapot margin eliminated | Active |

| Iran | Twelve-Day War; nuclear strikes | ~1.38 mbpd disrupted; 13.4% of seaborne imports | Active |

| Russia | Rosneft/Lukoil sanctions; secondary threat | State buyers paused within 24 hours | Variable |

| Malacca | US/Indian naval dominance; Hormuz closure | >83% of oil imports at structural risk | Structural |

| Minerals | FORGE: 21+ bilateral MOUs signed | IRA circumvention routes contested | Accelerating |

| NATO | 5% GDP target by 2035; all 32 at 2%+ | European defence capital redirected | Confirmed |

| Canada/CUSMA | Carney EV deal with Beijing; CUSMA review | Western alignment broken; US leverage gained | Unfolding |

I. The Energy Squeeze

China’s independent teapot refineries were built on sanctioned crude from Venezuela, Iran, and Russia. The arbitrage was simple: buy at a discount imposed by Western sanctions, process at market-equivalent product prices, capture the spread. At its peak, that feedstock covered roughly 17–18% of China’s total oil imports. All three legs have now been disrupted within eighteen months.

Venezuela

Venezuela supplied approximately 600,000 barrels per day to China in late 2025; around 4% of total imports, with a significant portion flowing as debt repayment against an estimated US$10–12 billion in oil-for-loans financing. Following the removal of President Maduro and the imposition of a 25% tariff on countries importing Venezuelan crude, Chinese traders halted purchases immediately. The Trump administration stated that Venezuelan oil would flow only through channels consistent with US law. The teapot arbitrage on Venezuelan barrels was closed.

Iran

China absorbed more than 80% of Iran’s seaborne oil exports in 2025; approximately 1.38 million barrels per day, or 13.4% of its total seaborne imports. Joint US-Israeli strikes in June 2025 degraded Iran’s nuclear programme and air defence infrastructure. Iran’s retaliatory capability deteriorated sharply: post-strike action was limited to a single base strike against a US facility in Qatar, compared with over 330 drones and missiles launched in a single April 2024 engagement. Qatar temporarily suspended LNG production during the conflict, affecting approximately 14% of China’s LNG supply.

The second-order consequence bears equal weight. Iran invested heavily in Chinese-supplied solid-fuel ballistic missile components and air defence systems in preparation for a confrontation with the US and Israel. The inability of that investment to deter or produce meaningful retaliation is now visible data for every sovereign client evaluating Chinese weapons systems; from sub-Saharan Africa to Southeast Asia. The PLA’s defence export franchise has a credibility problem it will take years to recover.

Russia and the Waiver Complication

When Venezuela and Iran were disrupted, Russia remained as the fallback. In October 2025, Rosneft and Lukoil were sanctioned; the first direct US action against Russian energy majors in the second Trump term, with secondary sanctions opened against buyers and financing banks including Chinese institutions. China’s state oil companies paused Russian crude purchases within 24 hours.

| Dollar-system access remains a binding constraint on Chinese financial institution behaviour, regardless of Beijing’s stated de-dollarisation agenda. The 24-hour response time is the relevant data point. |

The episode has produced a complication worth noting plainly. With Hormuz effectively closed during the Iran conflict in March 2026, Treasury issued General License 134 authorising delivery of Russian crude already loaded on vessels, subsequently superseded by GL 134B on April 17 and extended to May 16. Critically, GL 134B also permits US dollar-denominated transactions on those shipments; a meaningful relaxation, since forcing Russian oil out of the dollar system had been one of the primary enforcement mechanisms. Treasury Secretary Bessent stated publicly on April 15 that the broader licence would not be renewed; it was renewed two days later.

The back-and-forth reflects the inherent tension between market stability and sustained sanctions enforcement, particularly when Hormuz closure removes the supply buffer that would otherwise absorb the pressure. Senators noted Russia’s oil revenues nearly doubled in March during the Hormuz disruption; France made clear Russia should not benefit from the Iran conflict.

The structural outcome remains unchanged regardless of waiver sequencing: of China’s top ten oil suppliers, two (Iran, Venezuela) are effectively eliminated; five (Saudi Arabia, Oman, UAE, Kuwait, Malaysia) are close US allies; and Russia remains under active secondary sanction threat with dollar-system access as the leverage mechanism. The below-market feedstock that defined the teapot refinery sector’s economics is gone as a structural input.

II. The Malacca Constraint

| Over 83% of China’s oil imports; approximately 16 million barrels per day, transit the Strait of Malacca, 2.8 kilometres wide at its narrowest point, under effective US and allied naval dominance. China is the world’s largest oil importer; the United States is a net exporter. |

The Malacca Dilemma has been a fixture of Chinese strategic anxiety since President Hu Jintao named it in 2003. In the twenty-three years since, China has invested in Myanmar pipelines, Gwadar port infrastructure, and Arctic routing options, and moved approximately zero structural oil volume away from the strait. That vulnerability just became considerably more concrete.

In October 2025, Trump and Malaysian Prime Minister Anwar signed a Comprehensive Strategic Partnership; the first elevation of the bilateral relationship since 2014, covering defence, supply chains, and strategic coordination, with Malaysia sitting on the northeastern bank of the strait. In April 2026, the US formalised a Major Defence Cooperation Partnership with Indonesia, which controls the southwestern flank, including a reported request for blanket US military aircraft overflight access through Indonesian airspace; effectively putting American surveillance and rapid-response capability directly over the passage. Indonesia, Malaysia, and Singapore collectively govern the strait. Washington now has formalised strategic partnerships with two of the three.

The timing is not incidental. The Indonesia deal was signed while US destroyers were simultaneously enforcing the Hormuz blockade in the Persian Gulf; both chokepoints under active US influence in the same week. China has been deploying research vessels and underwater sensor arrays around the Malacca approaches for years, trying to map its own contingency options. Those efforts now face a US-aligned partner on both banks. Over 83% of China’s seaborne oil imports transit this passage. There is no alternative route at scale, and the strategic position just shifted materially against Beijing.

III. Critical Minerals and Strategic Chokepoints

China controls approximately 70% of global rare earth mining; the United States holds 12%. The FORGE initiative; successor to the Minerals Security Partnership, produced eleven bilateral critical minerals frameworks in February 2026 alone, including Morocco, Argentina, Ecuador, Guinea, and the Philippines, following ten additional agreements in the preceding five months covering Australia, Japan, South Korea, Saudi Arabia, and Thailand.

Morocco illustrates the specificity of the contest and its reach beyond supply chains. Chinese companies invested in Moroccan critical mineral processing and EV battery manufacturing to exploit Morocco’s FTAs with the US and EU; a circumvention pathway allowing Chinese-origin inputs, processed in Morocco, to enter Western markets outside IRA restriction. The US bilateral framework closes that pathway. But the FORGE agreement with Morocco carries a dimension the mineral framing alone does not capture.

US recognition of Moroccan sovereignty over Western Sahara; reaffirmed under the second Trump term, combined with the bilateral strategic framework effectively anchors US positioning at the western entrance to the Mediterranean. Morocco controls the southern bank of the Strait of Gibraltar, approximately 14 kilometres wide at its narrowest. Spain’s competing claims over Ceuta and Melilla create friction within the NATO alliance that the direct US-Morocco relationship partially bypasses. The agreement achieves three things simultaneously: it secures critical mineral supply chains, it closes Chinese circumvention routes through Moroccan re-export, and it places a US-aligned sovereign at the chokepoint connecting the Atlantic to the Mediterranean; the western bookend to Hormuz and Malacca.

| Washington now has influence over sovereign territory adjacent to three of the world’s most strategically significant maritime chokepoints: Hormuz (through Gulf ally relationships), Malacca (through US Navy and QUAD positioning), and Gibraltar (through the Morocco bilateral). China has influence over none of them. |

For China, which had been deepening commercial ties with Morocco precisely because of its position as a logistics and transshipment hub bridging Atlantic and Mediterranean trade lanes, the bilateral framework constrains both axes simultaneously: the supply chain architecture and the maritime access logic. The FORGE agreements contest both China’s primary supply chain positions and the circumvention architecture built to work around them with a strategic maritime overlay that extends well beyond the mineral framing in which it was announced.

IV. NATO — Structural Rearmament

All thirty-two NATO members agreed at the June 2025 Summit to raise the defence spending benchmark from 2% of GDP to 5% by 2035; the most significant commitment in the alliance’s history. All members are expected to reach the legacy 2% threshold for the first time in 2025; in 2023 only ten did. Germany will spend over €150 billion annually by 2029, more than double its 2021 level. NATO Europe and Canada accounted for 28% of total alliance spending in 2015; that share reached 38% in 2025.

A rearming Europe is reorienting industrial policy away from Russian energy dependence and Chinese dual-use technology exposure simultaneously. Defence procurement redirected to Western industrial capacity is capital unavailable to subsidise commercial relationships with Chinese-aligned supply chains. At 5% of European GDP, the magnitude over the following decade is material.

V. Canada and CUSMA

The Canada-US relationship heading into CUSMA renegotiation carries a pattern of friction that goes beyond the EV deal. Since taking office in March 2025, Prime Minister Carney has consistently positioned himself on the opposite side of Trump administration priorities in ways that have accumulated into a structural negotiating deficit. Canada imposed retaliatory tariffs on US goods following Trump’s March 2025 tariff action; a defensible response, but one that drew a direct escalation to 35% in August when Trump cited supply management in dairy and insufficient fentanyl interdiction.

Carney’s ‘Canada is not for sale’ declaration at the White House in May 2025, while domestically popular, was read in Washington as a confrontational posture rather than a negotiating position. Ontario aired an anti-Trump TV advertisement that caused Washington to cancel CUSMA talks entirely in October 2025. Talks only resumed in March 2026; five months lost in the lead-up to the July 1 mandatory review.

Into this already strained bilateral, Carney visited Beijing in January 2026 and cut the Chinese EV deal; reducing Canada’s tariff on Chinese EVs from 100% to 6.1% on an initial 49,000-vehicle quota, in exchange for China reducing canola duties from 84% to 15% and removing tariffs on canola meal, lobster, and crab through 2026. The optics were precise: a Canadian prime minister who had spent months publicly resisting Trump’s trade pressure was photographed in the Great Hall of the People the week before CUSMA renegotiation formally opened. The Trump administration responded directly; senior officials warned the Beijing deal could upend the CUSMA review, and Trump posted that China was ‘successfully and completely taking over’ Canada.

The substantive consequence is significant. CUSMA contains an explicit provision prohibiting partner nations from entering free-trade agreements with non-market economies such as China; Canada’s trade minister argued the Beijing deal was narrowly compliant, but the argument had to be made at all, in the week the review was opening, to a counterparty already sceptical of Canadian reliability. Every auto-sector chapter; the commercial heart of the deal, is now complicated: the US enters renegotiation focused on EV rules of origin and ensuring Chinese vehicles cannot access the US market via Canadian production, and Canada has just made a concession in exactly that domain.

Canada’s 77% export exposure to the US market defines the leverage asymmetry. Its resource endowment; energy, potash, uranium, critical minerals, provides substantial underlying leverage that a decade of infrastructure decisions has left partially unconverted. The LNG build-out that would have provided independent Asian market access at exactly the moment it is most needed does not exist. Canada arrives at its most consequential trade negotiation in a generation having systematically narrowed its room for manoeuvre.

VI. China’s Domestic Constraints

The external pressures above operate against a domestic economy not absorbing shocks from a position of strength.

| United States | China | Direction | |

| Nominal GDP (2025E) | $28.3T | $17.7T | Gap widening |

| GDP growth (2026F) | ~2.5% | 4.5% (Fitch: 4.1%) | Slowing vs. target |

| Real estate drag on GDP | — | –2.0 ppts (2024–25) | No recovery |

| Fixed asset investment | Positive | First annual decline (3 dec.) | Structural inflection |

| Oil import dependency | Net exporter | >15 mbpd imported | Acute exposure |

China’s property sector subtracted an estimated 2 percentage points from GDP growth in both 2024 and 2025 (Goldman Sachs). Real estate and infrastructure represent over 31% of GDP; a strong recovery is not forecast for 2026. Exports accounted for a third of 2025 growth (the highest share since 1997) masking weak domestic demand: retail sales grew 0.9% in December, and fixed asset investment posted its first annual decline in three decades of data. Fitch projects 4.1% GDP growth in 2026. Manufacturing supply chains are migrating incrementally to Vietnam, India, Mexico, and Eastern Europe in ways that are structurally difficult to reverse.

VII. Investment Implications

The GDP divergence in Figure 1 reflects both China’s domestic structural constraints and an external compression that compounds them. The conditions described; disrupted energy supply across three sources simultaneously, maritime chokepoints live-tested, mineral circumvention contested, proxy defence credibility damaged, NATO commitments locked in, and Canada’s CUSMA position weakened, do not resolve quickly. The gap is more likely to widen than narrow over the medium term.

International Oil M&A

The simultaneous disruption of three sanctioned crude supply lines; combined with the structural removal of the discount barrel from the teapot refinery model, is likely to trigger a re-rating of conventional oil asset values across frontier and emerging market jurisdictions. When China was the marginal buyer of Iranian, Venezuelan, and Russian crude at a steep discount, it depressed the market-clearing price for comparable heavy sour barrels and suppressed M&A appetite for assets in sanctioned or near-sanctioned jurisdictions. That dynamic is unwinding.

Sovereign buyers facing long-term energy security mandates; including sovereign wealth funds across the Gulf, Asia, and Europe, will need to replace the optionality that sanctioned crude provided with direct upstream equity stakes in compliant jurisdictions.

This points to an accelerating M&A cycle in international oil: Latin American heavy crude producers (Colombia, Ecuador, Brazil pre-salt), West African deepwater (Nigeria, Senegal, Namibia), and Gulf of Mexico mid-caps with uncontracted production are likely to attract premium valuations. Sellers in these jurisdictions who have been marking assets at discount to NAV under the assumption that Chinese national oil companies were the only credible strategic acquirors should revisit that assumption; the buyer universe has broadened materially as Chinese NOC participation becomes politically and legally more complex.

The parallel dynamic is the re-entry of Western majors into assets they divested under ESG pressure between 2017 and 2023, now reframed as energy security rather than carbon exposure. M&A advisory mandates in international upstream, midstream infrastructure, and LNG liquefaction capacity should be a direct beneficiary.

Structural Tailwinds — A Broader Map

The compression on China’s strategic position forces pivots across multiple sectors simultaneously. Each pivot creates a structural tailwind in the corresponding Western market:

Energy security infrastructure

- LNG infrastructure LNG export terminals and regasification capacity: the EU’s accelerated gas independence programme, combined with Asia-Pacific sovereign buyers replacing sanctioned crude with cleaner LNG, creates a sustained build-out cycle. US Gulf Coast, Australian, and Canadian LNG projects with FID or near-FID status are the most direct beneficiaries. Floating storage and regasification units (FSRUs) are capital-light and fast-to-deploy; the order book will expand.

- Midstream Midstream pipeline and tanker capacity: the rerouting of global crude flows away from sanctioned channels and through compliant jurisdictions requires incremental transport infrastructure. Jones Act tankers, VLCC operators with compliant flag registry, and pipeline companies serving non-sanctioned heavy sour corridors will see demand repricing.

Defence and dual-use technology

- Munitions Munitions manufacturing and replenishment: NATO’s structural rearmament requires restocking inventories drawn down by Ukraine transfers. Precision-guided munitions, artillery shells, and missile components are in multi-year supply deficit against committed procurement budgets. The Calgary munitions corridor is directly relevant.

- C4ISR Satellite and C4ISR systems: the demonstrated failure of Iranian radar and air defence against US-Israeli strikes will accelerate allied spending on surveillance, targeting, and communications infrastructure. Sovereign buyers across the Gulf and Asia are repricing the value of interoperable Western C4ISR against Chinese alternatives.

- Naval Shipbuilding and naval maintenance: the PLAN’s quantitative advantage in hulls does not translate to qualitative dominance in propulsion, electronics, or blue-water endurance. Allied navies in the Indo-Pacific are expanding procurement. South Korean and Japanese shipyards with naval division capacity are constrained; Australian and Canadian maintenance facilities are strategically positioned.

Critical minerals and processing

- Antimony / Tungsten Antimony and tungsten: both are Chinese-dominated supply chains with direct defence applications (hardeners for armour-piercing ammunition, filaments for electronics). The Lake George Antimony Project and Mount Pleasant Tungsten-Indium Deposit in New Brunswick are among the most shovel-ready Western-jurisdiction alternatives. Offtake interest from defence ministries is a structural demand driver rather than a commodity cycle call.

- Uranium Uranium and nuclear fuel: China’s domestic nuclear build-out continues regardless of Western sanctions, but Western utilities are simultaneously accelerating uranium procurement to diversify away from Russian-processed fuel. Kazakh and African uranium producers accessible to Western buyers, and Canadian in-situ recovery projects, are repricing toward energy security valuations rather than pure spot market economics.

- Rare earths Rare earth processing outside China: mining rare earths is well understood; separating and processing them at commercial scale outside China is not. MP Materials (US), Lynas (Australia), and emerging Canadian and Greenlandic projects are the only credible near-term alternatives. Capital for midstream separation and alloying facilities is the bottleneck; strategic equity is flowing.

- Phosphate Phosphate: Morocco controls approximately 72% of global reserves. The bilateral US-Morocco FORGE framework explicitly targets phosphate supply chain integration. Offtake agreements and equity stakes in Moroccan phosphate processing — relevant to both fertiliser security and battery cathode chemistry — will attract sovereign capital.

Financial infrastructure and trade finance

- Settlement Non-dollar settlement and SWIFT alternatives: Beijing’s response to dollar-system pressure has been to accelerate CIPS (Cross-Border Interbank Payment System) and RMB internationalisation. This creates demand for compliance, correspondent banking, and settlement infrastructure in jurisdictions that bridge both systems. Banks with established presence in both Western and Gulf markets are positioned as indispensable intermediaries.

- Trade finance Trade finance for realigned supply chains: as manufacturing migrates from China to Vietnam, India, Mexico, and Eastern Europe, the trade finance structures servicing those supply chains must follow. Working capital facilities, supply chain finance platforms, and credit risk transfer instruments for emerging market manufacturing corridors represent a decade-long origination cycle.

Food and agricultural security

- Agri-logistics Protein and grain logistics: China’s long-term agricultural vulnerability — arable land per capita among the lowest in the G20, water stress worsening, population still large — makes it a structural long-term buyer of protein, oilseeds, and grain from compliant jurisdictions. Brazil, Canada, and Australia are the beneficiaries. Infrastructure enabling secure, diversified agricultural export corridors — port capacity, grain storage, refrigerated logistics — will attract sovereign co-investment.

- Potash / Fertiliser Fertiliser supply chains: the disruption of Russian and Belarusian potash — which supplied approximately 40% of global potash before 2022; has been partially absorbed by Canadian producers. Canpotex and Nutrien have pricing power that will persist structurally as Chinese food security policy drives domestic consumption and Western sanctions constrain alternative suppliers. The Canada-China canola deal is a symptom of exactly this dynamic: Beijing buying agricultural insurance.

About Moneta

Moneta is an investment banking firm that specializes in advising growth stage companies through transformational changes including major transactions such as mergers and acquisitions, private placements, public offerings, obtaining debt, structure optimization, and other capital markets and divestiture / liquidity events. Additionally, and on a selective basis, we support pre-cash-flow companies to fulfill their project finance needs.

We are proud to be a female-founded and led Canadian firm. Our head office is located in Vancouver, and we have presence in Calgary, Edmonton, and Toronto, as well as representation in Europe and the Middle East. Our partners bring decades of experience across a wide variety of sectors which enables us to deliver exceptional results for our clients in realizing their capital markets and strategic goals. Our partners are supported by a team of some of Canada’s most qualified associates, analysts, and admin personnel.