Three prior cycles. The same structural logic each time. The opening transaction for the third has just been done.

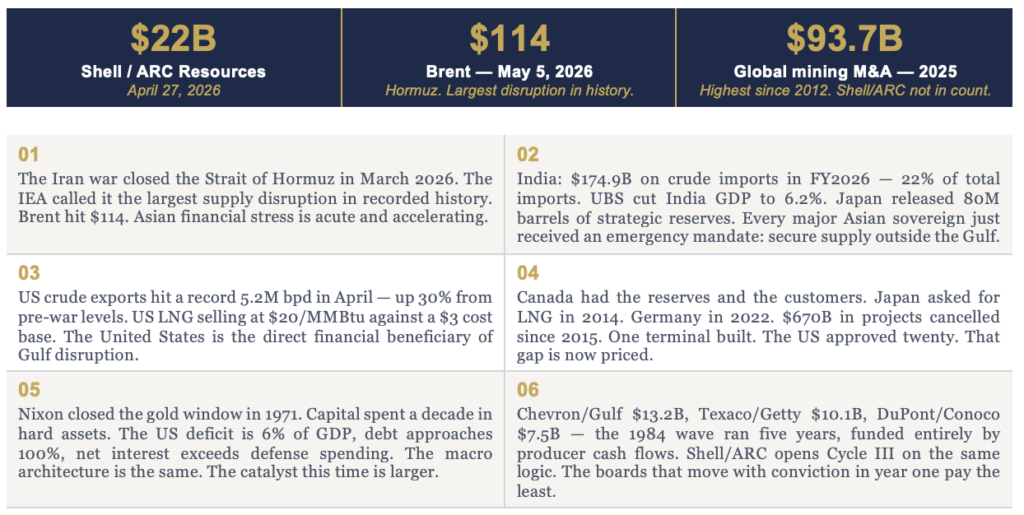

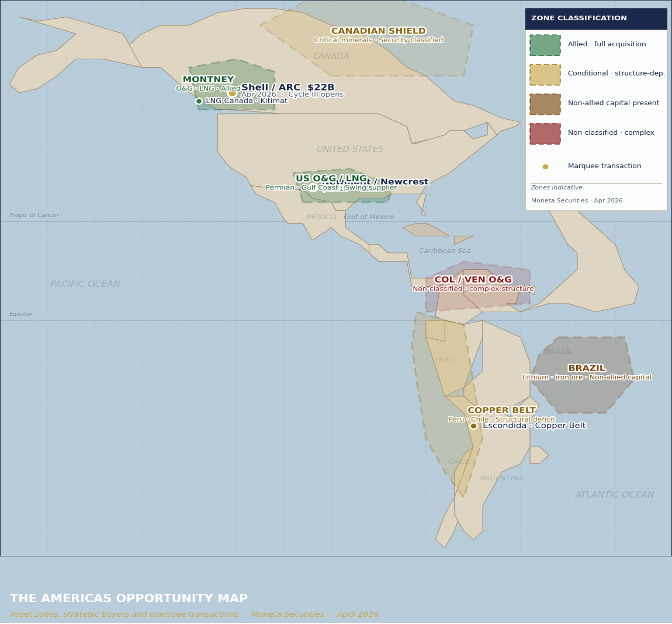

THE TRADE | Acquirer Map and Where the Premium Lives

Green = active buyer | Amber = conditional / structure-dependent | Red = restricted or resolution required. Premiums to unaffected market price are indicative and commodity-price dependent — in a sustained hard asset rotation, historical acquisition ranges do not define a ceiling. Canada note: US energy assets currently command an execution premium over Canadian equivalents pending regulatory normalisation. Moneta Securities analysis.

I. THE THESIS: CAPITAL IS LEAVING PAPER

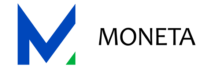

Resource M&A supercycles are capital allocation events, not commodity price events. When paper assets lose credibility as stores of value, capital moves into the ground. It has done this three times in the past fifty years. The current cycle has the same architecture as the prior two, with one difference: three structural forcing conditions are converging simultaneously. The Iran war is not the thesis — it is the accelerant that collapsed into sixty days a sovereign capital reallocation that would otherwise have taken three years. The opening transaction has just set the benchmark.

I. Fiscal debasement of the reserve currency creates structural demand for real asset stores of value. US deficit at 6% of GDP, debt approaching 100%, net interest exceeding defense spending. This condition has been building for a decade.

II. Supply disruption forces resource-importing sovereigns to reclassify energy and critical mineral security as a balance-sheet problem, not a procurement problem. The Strait of Hormuz closure made this explicit in March 2026.

III. Producer free cash flow at cycle highs funds acquisitions without the banking system. In 1984, Chevron did not need a syndicate. In 2026, Shell did not either. The capital is already inside the industry.

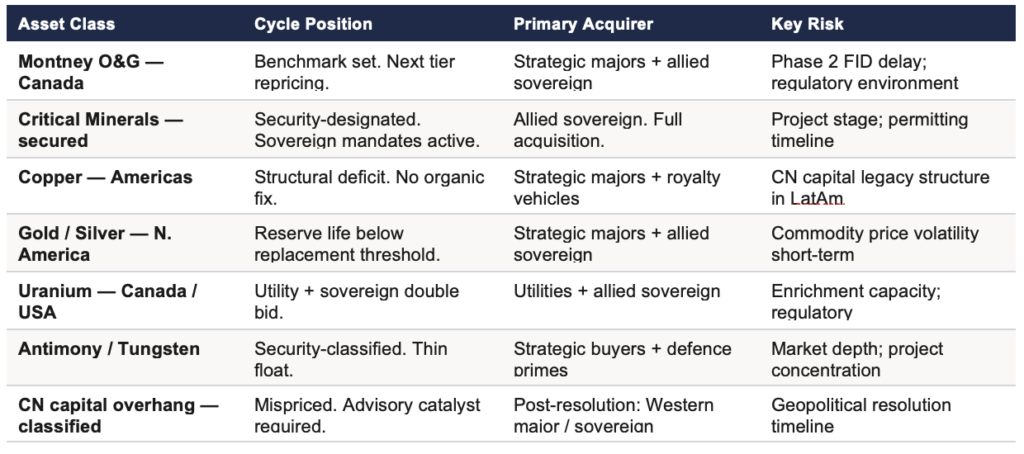

Cycle III has two features that prior cycles lacked. The acquirer map has been restructured by geopolitics: allied sovereign capital (ADIA, Mubadala, JBIC, JOGMEC, Saudi PIF) now has explicit policy welcome in the Western Hemisphere at a scale without prior-cycle analogue, with fifty-year time horizons and mandates across the full capital stack. The supply security imperative has also widened beyond energy to the full critical minerals chain; the materials required for energy transition infrastructure that every major economy has committed to build. The depletion problem driving M&A is not a single commodity.

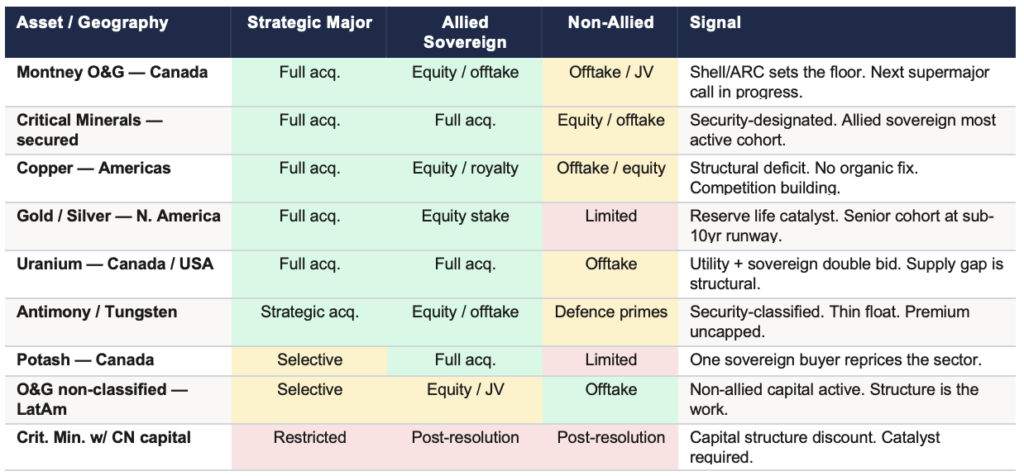

II. FIFTY YEARS, THREE WAVES, ONE LOGIC

The three resource M&A supercycles of the past half-century were triggered by different events but driven by the same underlying logic: reserve life in the major producers falls below the threshold where organic replacement is credible; balance sheets are strong enough to move; a macro event creates the urgency or the permission. A marquee transaction sets the benchmark and reprices the sector. Each wave lasted five to ten years.

The three resource M&A supercycles of the past half-century were triggered by different events but driven by the same underlying logic: reserve life in the major producers falls below the threshold where organic replacement is credible; balance sheets are strong enough to move; a macro event creates the urgency or the permission. A marquee transaction sets the benchmark and reprices the sector. Each wave lasted five to ten years.

Sources: FTC Petroleum Mergers; PwC Global Mining Deals; White & Case M&A Explorer; BOE Report; company filings. Cycle I premiums approximate to pre-announcement trading. Values not inflation-adjusted.

Three observations hold across all three cycles. The opening transaction is always read as an outlier; Shell at 27 percent into a clean process is this cycle’s DuPont/Conoco. The opening premium becomes the floor; boards that move in year one pay less than those who wait for the auction. The financing is always internal: producer free cash flow, not the banking system. Nine to thirteen percent FCF yields across the major producers today.

III. THE FORCING FUNCTIONS: WHY THIS CYCLE RUNS LONG

Five forcing functions are converging simultaneously. Three are structural — in place before the Iran war, unchanged after any resolution. Two are acute. Prior cycles had one. That is why this one runs longer.

1. Fiscal Debasement

US deficit at 6% of GDP; nearly double the fifty-year average. Net interest in FY2024: $882 billion, more than the defense budget. The analogue is exact: Nixon closed the gold window in 1971 and capital spent the following decade in the ground. The reserve currency is again under structural pressure from accumulated deficit weight, not a discrete event. Capital priced in paper for forty years is looking for the ground.

2. The Iran War

On March 4, 2026, Iran closed the Strait of Hormuz. Twenty percent of global oil supply disrupted; the IEA called it the largest supply disruption in recorded history. Brent moved 55 percent in four weeks. India spent $174.9B on crude imports in FY2026. Japan released 80 million barrels of strategic reserves. JPMorgan estimates only 800 million barrels of global storage are accessible without operational stress; 280 million have already been deployed.

The strategic consequence: every Asian sovereign fund inclined toward Americas resource security now has an emergency mandate to accelerate. LNG Canada is selling into Asia at $20/MMBtu against a $3 cost base. US crude exports hit a record 5.2 million bpd in April. The United States is the world’s energy swing supplier. That cash flow funds M&A.

3. The Geopolitical Channel

The restructuring of US trade and security policy since 2025 created a formal channel directing allied sovereign capital toward Western Hemisphere resource assets; the Minerals Security Partnership, the Canada-US Critical Minerals Action Plan, bilateral frameworks with Japan, South Korea, Australia, and the Gulf states. Chinese capital has been tiered, not eliminated: CFIUS and the Investment Canada Act are hard barriers for security-classified assets; commercial assets remain active with added complexity. The allied sovereign buyer class now has explicit policy welcome at a scale without prior-cycle analogue.

4. Supply: The Empty Pipeline

Sixteen to nineteen years from greenfield discovery to production. The exploration cuts of 2013–2018 created a supply gap no corporate growth mandate can close on timeline. The juniors are carrying the inventory the majors need to acquire. The only question is price.

5. Producer Balance Sheets

Nine to thirteen percent free cash flow yields across the major producers. The capital is already inside the industry, choosing between buybacks and reserve life. When the reserve life clock is running at the levels currently observed across the senior cohort, the choice is straightforward. The 1984 wave was financed the same way.

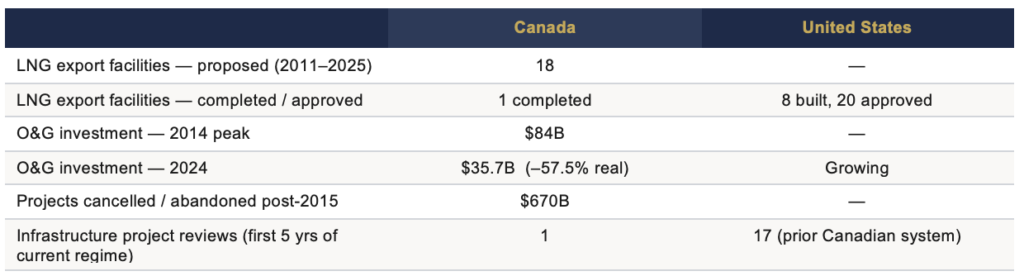

IV. CANADA: THE EXECUTION GAP

Canada has the reserves, the geography, and the allied-nation credentials to be the principal beneficiary of this cycle. The decade it had to build for that position, it spent debating whether to.

Japan asked for Canadian LNG in 2014. Germany asked in 2022 after Russia invaded Ukraine. Greece, Poland, and India asked. The answer, for a decade, was some variation of no business case, or decarbonisation transition, or no pipeline available.

The current government has declared Canada a leading LNG supplier while retaining Bill C-69 — one completed project review in five years against seventeen under the prior system — and a net-zero 2050 commitment. The aspiration and the policy architecture contradict each other. The market is resolving it.

LNG Canada Phase 1 is the most strategically positioned energy asset in the Western Hemisphere. Shell’s ARC acquisition is partly a bet on Phase 2 FID, which has not been taken. The position being underwritten in deal rooms is simpler: an acquirer with a long time horizon does not need Phase 2. It needs the gas that feeds the infrastructure already built. That sets the next tier of Montney producers as the natural acquisition target.

V. THE MISPRICED POSITION: CHINESE CAPITAL OVERHANG

Between 2012 and 2020, Chinese state capital took significant equity positions across the Americas resource sector (copper, gold, lithium, critical minerals) at a time when the capital was welcome and the returns were adequate. That capital is now structurally problematic. For security-classified commodities, a company carrying a Chinese state position cannot attract a Western strategic major or an allied sovereign without first resolving that position.

The asset is real. The project is advancing. The geology has not changed. The discount is entirely a capital structure problem, not an asset quality problem.

Latin America is the densest concentration of this mispricing; Peru, Chile, Colombia, and Brazil all attracted substantial Chinese involvement across copper, gold, and lithium. Companies carrying that legacy structure in classified commodities trade at a discount attributable entirely to ownership incompatibility. Resolving the position unlocks the deal.

For non-classified assets, Chinese capital can still participate and the opportunity is a structuring trade: an allied-friendly ownership architecture alongside an existing non-allied partner produces a materially larger buyer universe and a higher acquisition premium. The structure is the alpha.

VI. INVESTMENT IMPLICATIONS

Risks to the Thesis

Iran conflict resolution. A negotiated reopening of the Strait of Hormuz reduces the acute energy security urgency but does not alter the structural fiscal debasement thesis or the allied sovereign capital mandate. The cycle continues; the timeline lengthens.

Dollar resilience. If the US fiscal trajectory reverses materially — credible deficit reduction, debt stabilisation — the debasement thesis softens. There is no current policy trajectory that supports this scenario.

Canadian regulatory deterioration. Further tightening of project assessment in Canada widens the execution gap with the US and shifts acquisition premium to US-listed assets. The risk is real and partially reflected in current valuations.

Demand shock. A global recession driven by sustained high energy costs compresses the producer free cash flow that funds the wave. This is the primary scenario under which the cycle stalls. It has not materialized in either prior wave until the cycle was well advanced.

This report covers the Western Hemisphere opportunity. The same capital rotation is simultaneously opening a parallel set of trades in Sub-Saharan Africa, Central Asia, and parts of Southeast Asia — substantial resource inventory with none of the allied-alignment restrictions governing Western Hemisphere deal flow, at earlier-cycle valuations and with less competition. That is a different mandate and outside the scope of this analysis.

Prepared by Moneta Securities for informational purposes only. Not investment advice. Information believed reliable; no representation as to accuracy or completeness. Opinions as of April 2026, subject to change. Moneta Securities and affiliates may hold positions in or act as advisor to companies discussed. For sophisticated institutional and accredited investors only.

About Moneta

Moneta is an investment banking firm that specializes in advising growth stage companies through transformational changes including major transactions such as mergers and acquisitions, private placements, public offerings, obtaining debt, structure optimization, and other capital markets and divestiture / liquidity events. Additionally, and on a selective basis, we support pre-cash-flow companies to fulfill their project finance needs.

We are proud to be a female-founded and led Canadian firm. Our head office is located in Vancouver, and we have presence in Calgary, Edmonton, and Toronto, as well as representation in Europe and the Middle East. Our partners bring decades of experience across a wide variety of sectors which enables us to deliver exceptional results for our clients in realizing their capital markets and strategic goals. Our partners are supported by a team of some of Canada’s most qualified associates, analysts, and admin personnel.